Human Activities – My Study Level

The activities undertaken by human beings are known as human activities. A parson gets up in the morning and performs various activities during the day both at home and outside. A student may go to school, a worker may go to a factory, an employee may go to office, a businessman may go to his enterprise, others may take up their day to day work. All these activities in which we participate from morning till night are called human activities. On examining these activities, we may find that some activities produce direct economic benefits while others may not produce any direct economic benefits. Thus human activities may be classified into two categories:

1. Economic Activities

2. Non-Economic Activities

Economic activities are related to the production of wealth. Every human being undertakes some kind of work with a view to earn his living. All these activities create utilities. The aim of economic activities is to satisfy human wants. A worker goes to a factory for work, a farmer works in the field, a teacher teaches in the class, A doctor attends his patients, an advocate pleads in the court, all these activities are undertaken with a view to earn livelihood while doing some work. These activities enable persons to earn living and satisfy their wants. Economic activities are directed towards the satisfaction of human wants.

NON-ECONOMIC ACTIVITIES – Human Activities

These are those activities which are pursued for social, religious, cultural, psychological or sentimental reasons. Non-economic activities have no economic motive but are undertaken to have self satisfaction. These activities are voluntary in nature and are undertaken at the leisure or pleasure of the person pursuing them. The examples of such activities may be ; a housewife working at home, a person engaged in social work, attending a religious activity, listening to a discourse by a saint, attending to patients by volunteers, etc. All these activities are done for one’s own satisfaction.

Distinction between Economic and Non-Economic – Human Activities

| Basis | Economic Activities | Non – Economic Activities |

| 1. Meaning | These activities are undertaken to income to meet material needs. | These activities are of social and religious nature. |

| 2. Purpose | These activities are pursued with economic motive. They are undertaken for generation of income and wealth. Motives. | These activities are undertaken with social, cultural, religious and recreational motives. |

| 3. Scope | Activities may take place between employers and employees or between producers and consumers or between service providers and clients etc. | Non-economic activities may be among members of a family, social workers and those being served. |

| 4. Satisfaction | Economic needs of people are satisfied. | These satisfy social and psychological needs of the people. |

| 5. Money | These activities are measured in terms Measurement of money or money’s worth. | These activities have no money measurement. |

| 6. Type | These are related to business (industry

commerce and trade) profession and employment. |

These are family, social or religion related activities |

| 7. Examples | People are engaged in manufacture, trade, profession (doctor, advocate), service etc. | People are engaged in household trado , profession (doctor, advocate), activities, chantable work, social work, welfare activities, religious activities. |

TYPES OF ECONOMIC ACTIVITIES – Human Activities

(a) Profession

(b) Employment

(c) Business

PROFESSION : profession is an occupation which involves the rendering of personal service, of a specialized nature. The service is based on professional education, knowledge, teaching, etc. The specialized service is provided for a professional fee charged from the clients. The professionals are members of professional bodies of those lines and conduct their activities according to the standards set by those bodies. A person entering law profession has to obey the guidelines and regulations of Bar Council of India. A chartered accountant is governed by the Indian Institute of Chartered Accountants of India. Before joining a profession a person has to acquire the educational qualification set for that profession.

Features of a Profession

(1) A person entering a particular profession should have specialized knowledge and training prescribed for entering that profession. One must have a professional degree such as C.A., LL.B., M.B.B.S. etc. for entering a particular profession.

(ii) The membership of a particular professional body is compulsory before entering that profession. A Chartered Accountant must be a member of the Institute of Chartered Accountants of India and this is necessary for other professions also. (iii) Every professional body has a code of conduct which every member must follow. It contains norms of behavior for members.

(iv) Professionals charge fees from clients for providing their services.

(v) A professional cannot advertise himself if it is banned by the professional body.

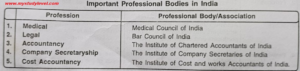

Important Professional Bodies in India

EMPLOYMENT OR SERVICE: When a person undertakes to render personal service under an agreement of employment, he is said to be in service or employment. The service is rendered for a salary or wage and/or

other benefits attached to that job. The service may be in a government or a private organization.

Features of Employment

(1) An employment commences when a person joins some organization for providing personal services.

(ii) There is a relationship of employer and employee. A person taking up a job is an

employee and the person who provides the service is called an employer.

(ii) The employer assigns duties to the employee. (iv) An employee is not required to make capital investment.

(v) The employees get salaries/wages for rendering their services to the organization.

(vi) The employee will have to follow service rules and regulations prescribed by the (vii) There are no standard qualifications for getting employment. The qualifications are linked to the requirements of particular jobs.

Leave a Reply